Your 20s can be a lot of fun. You might be travelling, figuring yourself out, maybe even making a mistake or two along the way. It happens.

But where you shouldn’t be making mistakes is with your finances and saving for retirement. Wait! hold up, thinking about retirement? In your 20s? It’s not as crazy as it sounds.

Having enough money to live on during retirement will likely be the largest financial goal of your life. How big? In order to live comfortably, experts agree you will want to live off 80% of your working salary.

To put that in perspective, if you retire making R750,000.00 a year, you would want to live off R600,000.00 annually.

In fact, in South Africa, the average retirement length is 18 years. So let’s multiply R600,000.00 by 18 years to get how much you should be having at the time of retirement. The answer would be R10.08 million.

However, that is just a rough estimate that doesn’t take into account factors like inflation, taxes, additional investment growth, or living longer than average, so you could need even more. This may sound daunting, but it’s more manageable than you may think.

You just need to start saving now. And not just saving, investing. That’s because of something called compound interest and it’s powerful.

Compound Interest Calculator

Compound interest is reinvesting earned interest back into the principal investment. As you reinvest interest on top of interest, your investments can grow on top of growth over time.

The idea can be a little abstract so let’s look at a quick example. To achieve growth that builds on growth, you need time and regular contributions.

If you invested R2,000.00 per week for 30 years with a 7% rate of return, you would end up with R10.12 million, more than the R10.08 million you would need from our previous example.

Keep in mind, if you are in your 20s and want to retire in your 60s, you would have 40 years, so even more time for growth. Of that money, only R3,120,000.00 would be your own contributions.

The other R7,000,000.00 would be due to compound interest. Sounds powerful, right? The takeaway is that in your 20s you have something on your side: time.

You are likely the furthest from retiring than you will ever be, leaving you with more time to reinvest and able to have your money make money, which can then make more money.

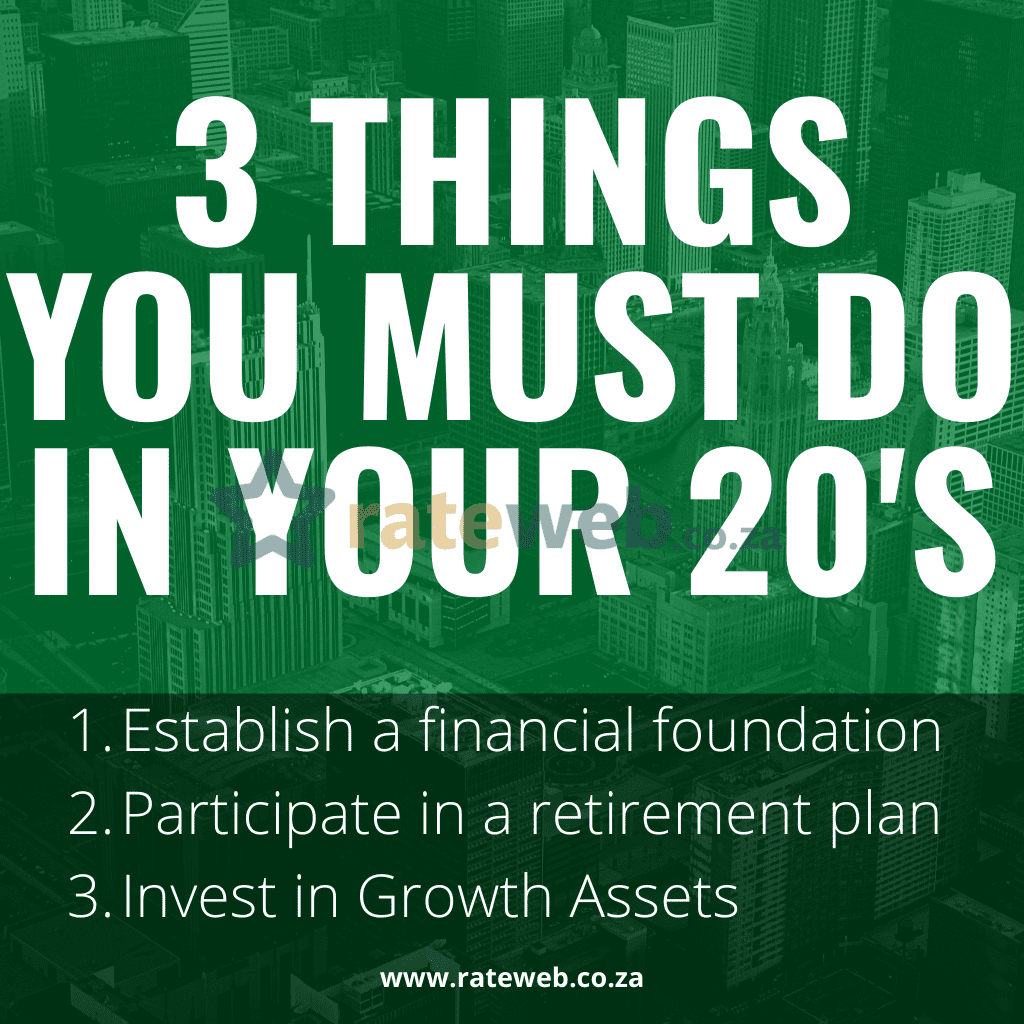

With that in mind, here are three things you need to do in your 20s: establish your financial foundation, participate in a retirement plan, and consider investing in assets that have a strong track record of growth, like stocks.

3 things you need to do in your 20s

1. Establish a Financial Foundation

The first step in your 20s is to establish your financial foundation, stuff you need to do to get ready to invest. To do that, you will want to save up an emergency fund of three to six months’ worth of expenses.

This cushion will help keep you from having to raid your retirement savings if your car breaks down or you find yourself without a job for a few months.

The other part of the foundation is to pay off any high interest debt, that is debt with an annual interest rate higher than 5%.

Debt with a rate this high would likely grow faster than most investments, so you’ve got to take care of it, or your money will never flourish.

It’s also a good idea to focus on your career in your 20s, trying to improve your potential for earnings.

It’s tough to save on an entry-level salary, so working on making more will make saving easier and your retirement goals more attainable.

2. Participate in a retirement plan

Once you get those obstacles out of the way, you can really focus on setting aside 15% of your income for retirement, which is typically your top investing priority. If you can’t save 15%, you are not alone.

Most South Africans contribute less than 10% of their annual salary to their retirement. 15% is a lofty goal, but if you are able to meet that mark, it will make saving for retirement that much easier.

A good goal is to have a year’s salary saved toward your retirement by age 30. The second step is deciding where to actually put all that money so it can grow.

There are types of accounts designed specifically for retirement investing that can provide potential tax benefits, which can help your money grow faster.

For example, Tax-free savings accounts (TSFA) and Retirement Annuities are retirement savings plans with tax breaks.

They allow you to set aside money from your salary, with tax-deferred. Of course, distributions during retirement will be subject to ordinary income tax. Some employers even offer matching contributions, furthering your growth potential.

3. Invest in Growth Assets

The third step is determining what to invest your money in. JSE Stocks can be risky, they can and do lose value sometimes. However, with that risk comes the potential for growth.

One rand invested in large stocks in 1926 would have been worth more than R9,000.00 by the end of 2019, even with some market crashes along the way.

Your 20s are the decade where your tolerance for risk is typically the highest because you have the most time to recover from a market downturn.

So, an investor in this age range might look to build and maintain a portfolio where 90% of assets are in stocks and 10% are in something safer like bonds.

Just make sure you never stop seeking diversification. For example, index funds are a type of investment that allows you to spread your money across hundreds of stocks or bonds.

If you want to pick individual stocks, make sure you are looking at different sectors, company sizes, and countries, in other words, don’t put all your eggs in one basket. For instance, investing in South African stocks only may not be a good idea. You need to diversify.

Of course, make sure the ratio of stocks to bonds is in line with your own risk tolerance. The 90 to 10 ratio is not necessarily going to be appropriate for everyone in their 20s.

If you have more risk tolerance you can even look at investing a portion of your money into Cryptocurrencies like Bitcoin, Ethereum, Cardano and Polkadot. The crypto market comes with high risk because it hasn’t fully matured. However, it presents a good risk to reward ratio. And as it matures, it will become much safer.

Conclusion

To recap, your 20s are meant to be enjoyed but be sure you’re also setting yourself up for the future. Establish a solid financial foundation by creating an emergency fund and paying off any high-interest debt you have.

Also, make sure you are taking advantage of the power of compounding by enrolling in some kind of retirement plan. And finally, seek growth-orientated investments while you are still young enough to recover in the event of a downturn.

Taking steps now can help you set yourself up for a comfortable retirement. Trust me, your 65-year-old-self will thank you.